Publications

Letter from the CIO - May 2026

Back to normal… or almost

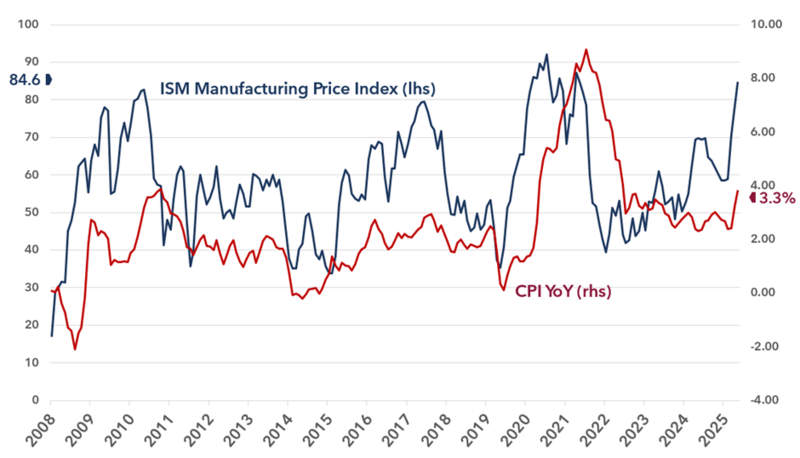

Financial markets continued their recovery in May, against a backdrop of gradually easing tensions following the geopolitical unrest in the Middle East. The ceasefire and reassuring messages from the US administration enabled investors to quickly return to riskier assets, giving the markets the appearance of a return to normal… or almost. In the United States, the S&P 500 has now risen by nearly 15% from its April lows, whilst the Nasdaq has risen by more than 25%, buoyed by a particularly strong first-quarter earnings season and an earnings outlook that remains favourable for the whole of 2026. The technology sector, small caps and, more broadly, growth stocks have rebounded strongly, with US small-cap indices rising by nearly 15% over the month. Emerging markets are also part of this trend, having risen by nearly 25% from their lows, benefiting from a return of risk appetite and a slightly weaker dollar. This return to a “risk-on” stance is, however, taking place against a macroeconomic backdrop that is more contrasted than the current momentum in the financial markets would suggest. The latest inflation figures confirm a gradual rise in inflationary pressures, with US inflation, in aggregate terms, once again rising above 3%, putting renewed pressure on US and European government bond yields. The yield on the 10-year US Treasury is now hovering around 4.4%, reflecting a market that continues to anticipate a cautious Federal Reserve and persistently high policy rates. In the credit markets, however, this rise in long-term rates has been partially offset by the resilience of the Investment Grade and High Yield segments, which have benefited from a further narrowing of spreads. After rising by more than 15% in April, oil prices have recently eased on the back of ongoing talks between the US and Iran, reinforcing this sense of a gradual normalisation of financial markets. A resilient economy but persistent inflationary pressures The macroeconomic picture remains more contrasted than the current momentum in the financial markets suggests. The US economy continues to show remarkable resilience, underpinned by robust consumption, a still-strong labour market and a gradual improvement in manufacturing activity. In the US, the ISM Manufacturing index remained in expansionary territory at 52.7 in April, whilst in Europe, the eurozone manufacturing PMI rose to 52.2 from 51.6 the previous month, confirming a gradual improvement in the industrial cycle. This recovery remains supported in particular by the rebound in new orders, exports and restocking effects. The US labour market remains resilient overall. Non-farm payrolls rose by 115,000 in April, whilst the unemployment rate remained stable at 4.3%. At the same time, US GDP for the first quarter came in at close to 2% on an annualised basis, following a particularly weak final quarter of 2025, confirming the resilience of the US economy despite a more uncertain environment. This resilience is, however, accompanied by a gradual rise in inflationary pressures. Price-related components in the US ISM Manufacturing index are rebounding sharply, with the prices paid index reaching 84.6, a level reminiscent of the pressures observed in 2022. Delivery times are also tightening again, signalling persistent pressures on supply chains. The latest inflation figures confirm this trend: in the US, headline CPI inflation now stands at 3.3% and core CPI at 2.6%. In the eurozone, it stands at 3.0% and 2.2% respectively. Persistent energy pressures and logistical disruptions thus continue to fuel higher inflation expectations. Reacceleration in Manufacturing Prices and Inflation Risks  Source: Bloomberg / Banque Heritage

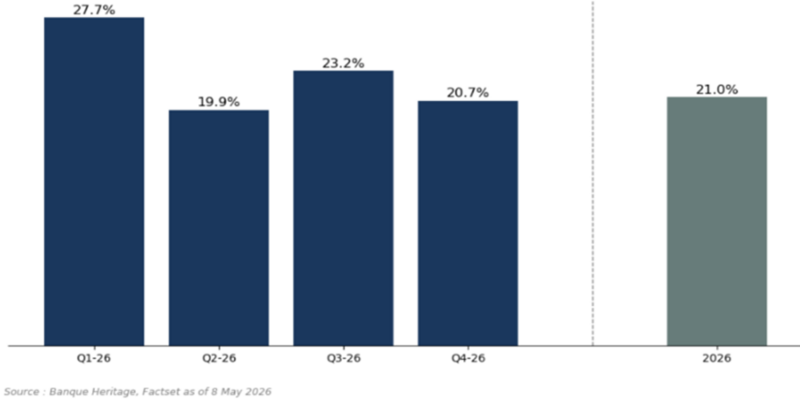

Against this backdrop, central banks are maintaining the status quo for the time being and have stated that they are prepared to adjust their monetary policy in line with forthcoming data. The cycle of monetary easing now appears to be over, whilst the outlook for monetary policy remains particularly uncertain. The US Federal Reserve finds itself facing a complex environment, marked both by an expected change in leadership as early as June and by an economy that remains resilient but is increasingly exposed to strong stagflationary pressures. Corporate earnings remain the market’s main driver Beyond macroeconomic and geopolitical developments, earnings momentum continues to be the main pillar underpinning equity markets, particularly in the United States. The 2026 first-quarter earnings season has once again confirmed the strong resilience of US companies. At this stage, nearly 89% of S&P 500 companies have reported their results, with around 82% beating earnings-per-share expectations. Aggregate earnings growth now stands at nearly 25%, the highest rate since 2021, whilst net margins remain close to 15%, a high not seen for over a decade. US EPS projections YoY

Source: Banque Heritage, Factset as of 8 May 2026 This momentum remains largely driven by the technology and communications services sectors, and more broadly by the entire artificial intelligence ecosystem. US tech giants continue to generate strong cash flow and are maintaining particularly high levels of investment in AI infrastructure, which is now central to market growth expectations. Financial firms have also reported solid results, supported in particular by trading revenues and the resilience of market activities. Despite persistently high interest rates, ongoing geopolitical tensions and rising energy costs, US companies continue to demonstrate a remarkable ability to adapt. The outlook for the rest of the year remains broadly positive, although earnings growth continues to be heavily concentrated among major US market leaders and sectors directly exposed to technology spending and artificial intelligence. Positioning: style rotation and fixed income diversification The coming months will continue to be driven primarily by four key macro-financial factors: economic growth, corporate earnings momentum, inflation trends and the trajectory of interest rates. Against this backdrop, we maintain an overall positive stance on risk assets, whilst avoiding any sense of euphoria following the sharp rebound seen since the April lows and in an environment where valuations have become more demanding in certain market segments. From a regional perspective, we continue to favour emerging markets, which are benefiting from a slightly weaker dollar, a gradual improvement in the global manufacturing cycle and valuation levels that remain attractive relative to developed markets. We are also gradually rotating towards more “value” segments in developed markets, as the valuation gap between growth stocks and undervalued stocks remains historically high. Finally, the current environment is gradually undermining the traditional 60/40 model, which is being penalised by the simultaneous rise in inflation and long-term interest rates. We therefore favour a more diversified fixed income portfolio, incorporating strategies that are more uncorrelated with traditional assets, such as inflation-linked bonds, Cat Bonds or certain segments of structured credit such as senior CLOs. |

May 13, 2026

Publications

Publications

BANQUE HERITAGE POSTS SOLID HALF-YEAR RESULTS IN ITS 40TH ANNIVERSARY YEARGeneva, 29 July 2026 – Banque Heritage announces strong half-year results, confirming the Bank's sustained growth trajectory.

July 29, 2026

Publications

OUTLOOK 2026 H2For more than a decade, investors operated in a world shaped by central banks: low inflation, abundant liquidity and ever-lower interest rates.

June 23, 2026

Publications

Letter from the CIO - April 2026Geopolitical Easing and Economic Resilience: A More Constructive Yet Still Uncertain Environment

April 16, 2026