Publications

Letter from the CIO - April 2026

Geopolitical Easing and Economic Resilience: A More Constructive Yet Still Uncertain Environment

• Oil prices fall, but markets remain supported despite ongoing uncertainty

• Inflation driven by energy costs, but core inflation remains broadly under control

• Divergence between households and markets, risks to consumption and credit conditions

A Geopolitical Easing Supporting Markets

After a month of March marked by a sharp escalation of tensions in the Middle East, the announcement of a ceasefire between the United States, Israel, and Iran has led to a gradual easing in financial markets. The energy risk premium, which had weighed heavily on risk assets, has begun to recede. Brent crude oil, which briefly reached around USD 115 per barrel at the end of March, is now trading below the USD 100 threshold, reflecting renewed optimism regarding a gradual normalisation of global energy flows. This easing, although fragile and relative, has supported a rebound in equity markets. After marked declines in March (approximately -5% for the S&P 500 and -9% for the Euro Stoxx 50), major indices have resumed a positive trajectory, in line with improving market sentiment. The S&P 500 is now slightly positive year-to-date. In currency markets, the US dollar, which had strengthened as a safe haven, with EUR/USD falling to 1.1415 in March, has since lost momentum following the ceasefire announcement. The pair is currently trading around 1.175, close to levels seen at the beginning of the year. While this easing is a positive development, caution remains warranted regarding its durability and strength. Negotiations are likely to be prolonged and subject to reversals, leaving a significant degree of geopolitical uncertainty.

A Global Economy Continuing to Show Resilience

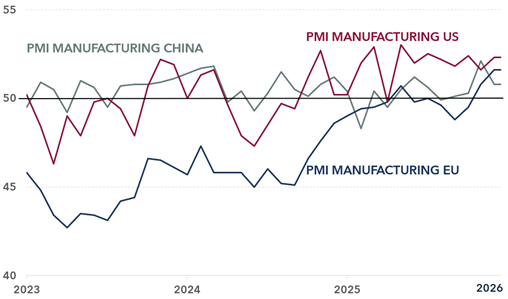

Beyond the geopolitical backdrop, macroeconomic data continue to reflect a broadly encouraging dynamic. In the United States, despite an ongoing normalisation phase, the labour market remains solid, with approximately 178,000 jobs created in March, exceeding expectations, and an unemployment rate holding around 4.3%. This confirms the resilience of the US economy, although the full impact of the recent energy shock may not yet be fully reflected. Some leading indicators point in the same direction. Manufacturing PMI indices rebounded simultaneously across the US, Europe, and China in March, signalling an improvement in global industrial activity, despite the recent rise in energy prices. While this trend should be interpreted with caution, it may suggest that the global economy is now less sensitive to oil shocks than in previous cycles.

S&P Global Manufacturing PMI Index

Source: Bloomberg / Banque Heritage

On the inflation front, pressures remain present but still contained in their underlying dynamics. Headline CPI stands at 3.3% year-on-year in March, accelerating from 2.4% in February, mainly driven by energy-related effects. On a monthly basis, prices increased by 0.9%, fuelled by a more than 10% rise in energy costs, with gasoline prices jumping by over 20%.

By contrast, core inflation remains more moderate. Core CPI stands at 2.6% year-on-year, with a limited 0.2% monthly increase, suggesting that second-round inflationary pressures remain contained for now. This divergence between headline and core inflation highlights the largely exogenous nature of the recent shock, driven by energy, rather than a broad-based inflation surge. Market-based inflation expectations have edged slightly higher, with the US 5-year breakeven rate around 2.4%–2.5%, reflecting a moderate reassessment of inflation risk without signs of de-anchoring.

Strong Earnings Outlook, Particularly in the United States

In this context, corporate earnings prospects remain well supported, particularly in the United States, where earnings growth is expected to reach around +16% by 2026, driven by favourable structural trends. US companies continue to benefit from powerful tailwinds, including productivity gains linked to artificial intelligence, asset-light business models, and sustained pricing power. Overall, US corporates remain in strong financial health, with profits representing approximately 14% of GDP, a historically elevated level that reflects the strength of the current earnings cycle.

At the same time, valuations have partially normalised following the elevated levels observed at the end of 2025. The valuation premium of US equities relative to Europe has declined to around 1.3x, close to its historical average. This adjustment has mainly been driven by a compression in US multiples rather than a re-rating of European markets, where growth prospects remain more limited. Earnings revisions further support this divergence: they are trending positively in the US, while remaining more mixed in Europe, weighed down by weaker growth, a stronger euro, and a sectoral composition that is more tilted towards traditional and cyclical industries (banking, energy, manufacturing).

Fragility Signals to Monitor Closely

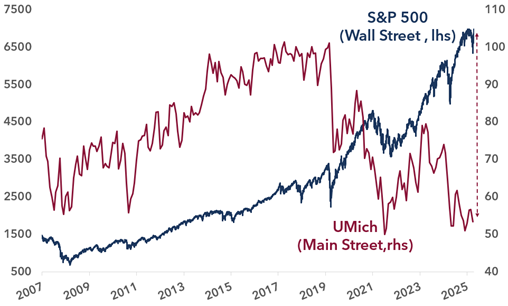

Despite these constructive elements, several indicators call for caution. US consumer confidence has deteriorated significantly, with the Michigan Consumer Sentiment Index falling to 47.6, a historical low. This reflects both geopolitical concerns and a gradual erosion of purchasing power in an environment shaped by several years of persistent inflation.

At the same time, short-term inflation expectations remain elevated, with projections at 4.8% over one year, suggesting that price pressures may not only persist but could also take time to normalize, particularly given the uncertainty surrounding a durable geopolitical resolution. The recent rise in headline CPI, largely driven by energy, could therefore continue to weigh on consumption in the coming months.

In this environment, the Federal Reserve is likely to maintain a restrictive monetary stance for longer than previously anticipated. The scenario of rate cuts is gradually fading, while the probability of further rate hikes has increased. US long-term yields are hovering around 4.30% on the 10-year Treasury, reflecting this reassessment of expectations.

Finally, the gap between household sentiment and financial market performance continues to widen. This imbalance, combined with potentially tighter financial conditions, could gradually weigh on consumption and credit, warranting a measured approach in the months ahead.

Main Street vs. Wall Street

Source: Bloomberg / Banque Heritage

Positioning: A Constructive Yet Still Clouded Environment

In this context, our central scenario remains one of a resilient global economy evolving towards a soft landing, supported by solid fundamentals and a recent easing in geopolitical tensions. Equity markets could benefit from a more supportive environment, underpinned by more balanced valuations, continued earnings growth, particularly in the United States, and favourable structural trends. In Europe, a sustained stabilisation in energy prices would also provide an additional tailwind for corporates.

However, several areas of uncertainty remain, including the trajectory of inflation, the direction of monetary policy, fragile consumer sentiment, and geopolitical uncertainties. These factors could continue to generate bouts of volatility in the months ahead. In this context, we maintain a balanced and measured approach, suited to an environment that remains constructive yet uncertain.

April 16, 2016

Publications

Publications

OUTLOOK 2026 H2For more than a decade, investors operated in a world shaped by central banks: low inflation, abundant liquidity and ever-lower interest rates.

June 23, 2026

Publications

Letter from the CIO - April 2026Geopolitical Easing and Economic Resilience: A More Constructive Yet Still Uncertain Environment

April 16, 2026