Publications

Geopolitical Shock in the Middle East: Short-term Volatility, Fundamentals Still Prevail

- Markets are pricing in an energy risk premium: oil is approaching USD 100. - Geopolitical crises have historically had a limited impact on markets. - Higher oil prices act as a global tax on consumption.

An Energy Risk Premium Driving Market Reactions

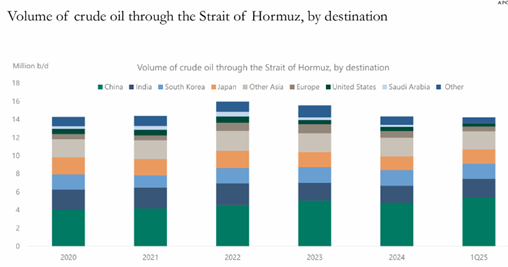

Geopolitical tensions in the Middle East have intensified significantly since the beginning of the conflict involving Iran, reigniting concerns about the stability of global energy flows. Markets have quickly priced in a significant risk premium, particularly visible in energy prices. Oil is now trading around USD 100 per barrel, its highest level since 2022. This reaction highlights the market’s extreme sensitivity to any potential disruption in the Strait of Hormuz, through which nearly 20% of the world’s oil supply transits. Any prolonged interruption in this area would represent a major shock to global supply.

Source: U.S. Energy Information Administration (EIA) analysis based on Vortexa, Apollo Chief Economist.

Financial markets have reacted in a manner typical of an oil shock, although it remains somewhat premature to label it as such. The dollar, which had been widely criticized in recent months, has quickly regained its safe-haven status; the Dollar Index has moved above the 100 mark and EUR/USD is now trading around 1.145, nearly three figures lower than before the conflict began. Gold, on the other hand, has surprised with its relative weakness. After an exceptional rally in recent months, the precious metal is trading slightly below USD 5,000 per ounce. Its already elevated valuation appears, for now, to be limiting additional investor inflows. Equity markets have seen a noticeable increase in volatility, but corrections remain relatively contained at this stage. The MSCI World index has declined by around 5% since the start of the conflict, the

S&P 500 by roughly 3.5%, while European markets are down close to 6%. Finally, in bond markets, rising inflation expectations linked to higher oil prices have pushed sovereign yields upward. The US 10-year Treasury yield is now trading around 4.30%, approximately 35 basis points above its level at the end of February.

Financial history nevertheless reminds us that geopolitical crises typically have a limited impact on markets over the medium term. Since the attack on Pearl Harbor in 1941, US equities have been higher twelve months after the onset of a crisis in nearly 75% of cases. In roughly half of those episodes, markets even recovered their initial levels in less than a month.

An Oil Shock Acting as a Global Tax on Consumption

Beyond the immediate market reaction, the key question concerns the macroeconomic impact of persistently higher oil prices. One way to understand this dynamic is to view rising energy prices as an implicit tax on consumers and businesses. In the United States, for example, an increase in gasoline prices from USD 2.80 to USD 3.50 per gallon is equivalent for households to a tax increase of roughly 70 cents per gallon. Unlike a traditional tax, however, these additional revenues do not accrue to governments but rather to energy producers, resulting in a transfer of income from consuming countries to producing countries.

Historically, a USD 10 increase in the price of oil tends to raise global inflation by around 0.2 to 0.3 percentage points and reduce global growth by approximately 0.1 to 0.2 percentage points of GDP. The magnitude of these effects varies significantly across regions.

The United States appears better positioned today than during previous energy cycles. Thanks to the development of shale oil, US production now exceeds 13 million barrels per day, making the country the world’s largest oil producer. This high level of production helps cushion the overall macroeconomic impact of an energy shock. It does not fully shield consumers, however, as domestic prices remain largely determined by global markets, resulting primarily in pressure on household purchasing power.

Europe, despite diversification efforts undertaken since the 2022 energy crisis, remains structurally more exposed to energy price fluctuations. European economies generally consume less oil per unit of GDP than the United States (France roughly one third, and the United Kingdom about half) but remain more vulnerable to the natural gas market, where prices can be two to four times higher than in the US due to logistical constraints in the global gas market.

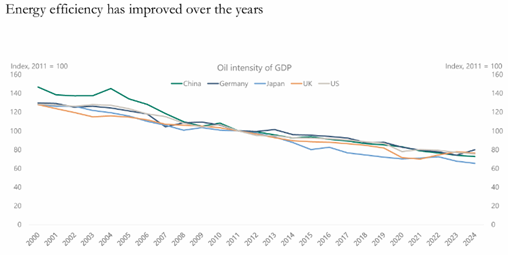

East Asian economies appear potentially the most exposed. Japan and South Korea rely heavily on energy imports and display relatively high energy intensity. South Korea, in particular, consumes more than twice as much oil per unit of GDP as the United States, making its economy especially sensitive to a prolonged energy shock. China appears somewhat better positioned thanks to a broader diversification of its energy supply and the significant role of domestic coal production. Nevertheless, as the world’s largest oil importer, it would remain exposed to a sustained increase in energy prices, which could weigh on industrial costs and overall economic momentum.

Source: BNEF, IMF, Apollo Chief Economist. Note: Oil burned per unit of GDP indexed to 2011.

In an extreme scenario where energy flows from the Middle East were to be durably disrupted, the impact on the global economy could become significant and increase the risk of an economic slowdown. In the absence of a prolonged disruption to global supply, however, an oil shock typically acts more as a temporary drag on growth than as a trigger for recession.

Positioning: Diversification and Protection Against Volatility

In this context, our central scenario remains that the current rise in oil prices primarily reflects a geopolitical risk premium rather than a structural disruption in global supply. Energy prices could therefore rise temporarily by an additional USD 20 to 30 before stabilizing if tensions remain contained. While a recession is not our base case at this stage, the risk of stagflation should not be underestimated. Higher energy prices could fuel inflationary pressures and weigh on household purchasing power, while a less accommodative monetary policy environment could also affect both households and businesses.

Such a scenario is currently under close evaluation within our teams and could, if necessary, lead to adjustments in our portfolios.

March 17, 2026

Publications

Publications

Affordability, America’s Achilles’ HeelIn an economy that remains wealthy yet increasingly fragmented, purchasing power has become Washington’s primary test.

February 13, 2026

Publications

Letter from the CIO - February 2026Markets in Transition: Fewer Obvious Trades, Greater Balance

February 12, 2026

Publications

Outlook 2026 H1The year 2025 confirmed a global soft-landing scenario, albeit at the cost of persistent imbalances across major economic regions.

January 15, 2026